Why “drill, baby, drill” won’t lower your utility bills

Increasing fracking and drilling operations could help energy companies, foreign consumers, tech companies, and shareholders— but not struggling Americans.

I wrote this post, which was originally published by the Ohio River Valley Institute. I’m resharing it here with The Public Good readers because I believe many will be interested in the topics discussed.

Cheap energy has always been good politics. Almost every American voter feels the pinch when heating and electric bills rise. Like the snake oil salesmen in the Old West, American politicians have always confidently sold too-good-to-be-true corporate concoctions and foreign policy poultices to cure our energy ailments.

The problem is that political slogans don’t capture the complex reality of reliably delivering energy to hundreds of millions of people on demand. For example, “energy independence” was once an evergreen applause line at the rallies of both major American political parties. As the governor of California in 1974, Ronald Reagan warned that failure to achieve energy independence would lead to “coercion and blackmail” by foreign adversaries. Thirty years later, in 2004, both Senator John Kerry (who would later become the Special Presidential Envoy for Climate in 2021) and his opponent, President George W. Bush, campaigned by promising to deliver energy independence.

It didn’t happen in 1974, nor in 2004. But by tapping into the popular and quintessentially American belief in self-sufficiency, the slogan of “energy independence” conveyed a tantalizing, albeit false, premise: if only America could wean itself off Middle Eastern oil, then our energy prices would automatically come down and our country would be somehow immune to the turmoil of foreign affairs.

Now, nearly half a century since the term was first in vogue, America has, against all odds, theoretically achieved energy independence. (In practice, technical refinery complications mean that we still need to effectively ‘swap’ our oil on the global market). We have become the world’s top oil and gas producer. But instead of getting cheaper, energy prices have stubbornly climbed higher for American households. Why?

Our last election was no different than 1974 or 2004 in this regard. “Unleashing American Energy” joined “energy independence” and “drill, baby, drill” as the latest slogan from the campaign trail. As a candidate in 2024, President Donald Trump promised that his policies would cut Americans’ utility bills in half within one year of his return to the White House. His administration has, uncreatively, worked to fulfill his promise by following a failed playbook for ramping up oil and gas production, even as the U.S. has already hit record levels of output.

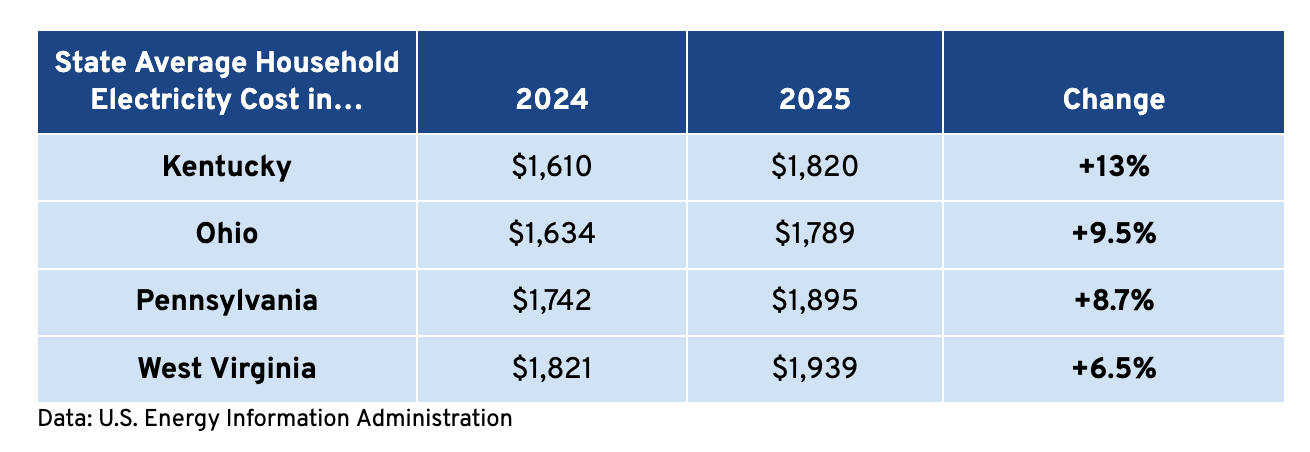

But despite the President pushing for even more fossil fuel extraction by fast-tracking oil and gas development on federal lands and proudly unveiling plans for giant new foreign-owned gas power plants, most of us are paying more for our utilities one year later, not less. My own natural gas bill rose by more than 25% in February as an arctic blast of bitter cold descended on much of the U.S., sending temperatures to near zero for several weeks. But beyond just weather, the story is much the same across the Ohio River Valley, where electricity and natural gas prices have soared in recent years under both Presidents Biden and Trump. Even West Virginians, who live in the heart of Appalachian gas and coal country, have had to sacrifice other basic needs to keep their lights and heat on.

How is it that America can be producing more energy than ever before, yet our utility bills continue to rise? And, more importantly, what is the likelihood that this administration will be able to deliver on its lofty campaign promise by sticking with its current policies?

It needs to be said upfront that our energy system is almost infinitely complex. It’s so complex, in fact, that you could spend a lifetime studying it and still not understand all of the intricacies and idiosyncrasies. One of the reasons I enjoy being an economist, though, is that even the most complex systems have to stand up to logical scrutiny and the basic forces that drive our economy. The numbers, so to speak, still have to add up, and incentive structures that politicians create with regulation and tax policy still need to align with real human behavior.

And, from this economist’s point of view, there are several glaring reasons to be doubtful about the ability of Washington’s new energy policies, touted as “unleashing American energy,” to deliver lower bills, and thus more disposable income, for Americans.

1. Exporting more liquified natural gas (LNG) puts Americans in direct competition with foreign consumers for gas, raising prices.

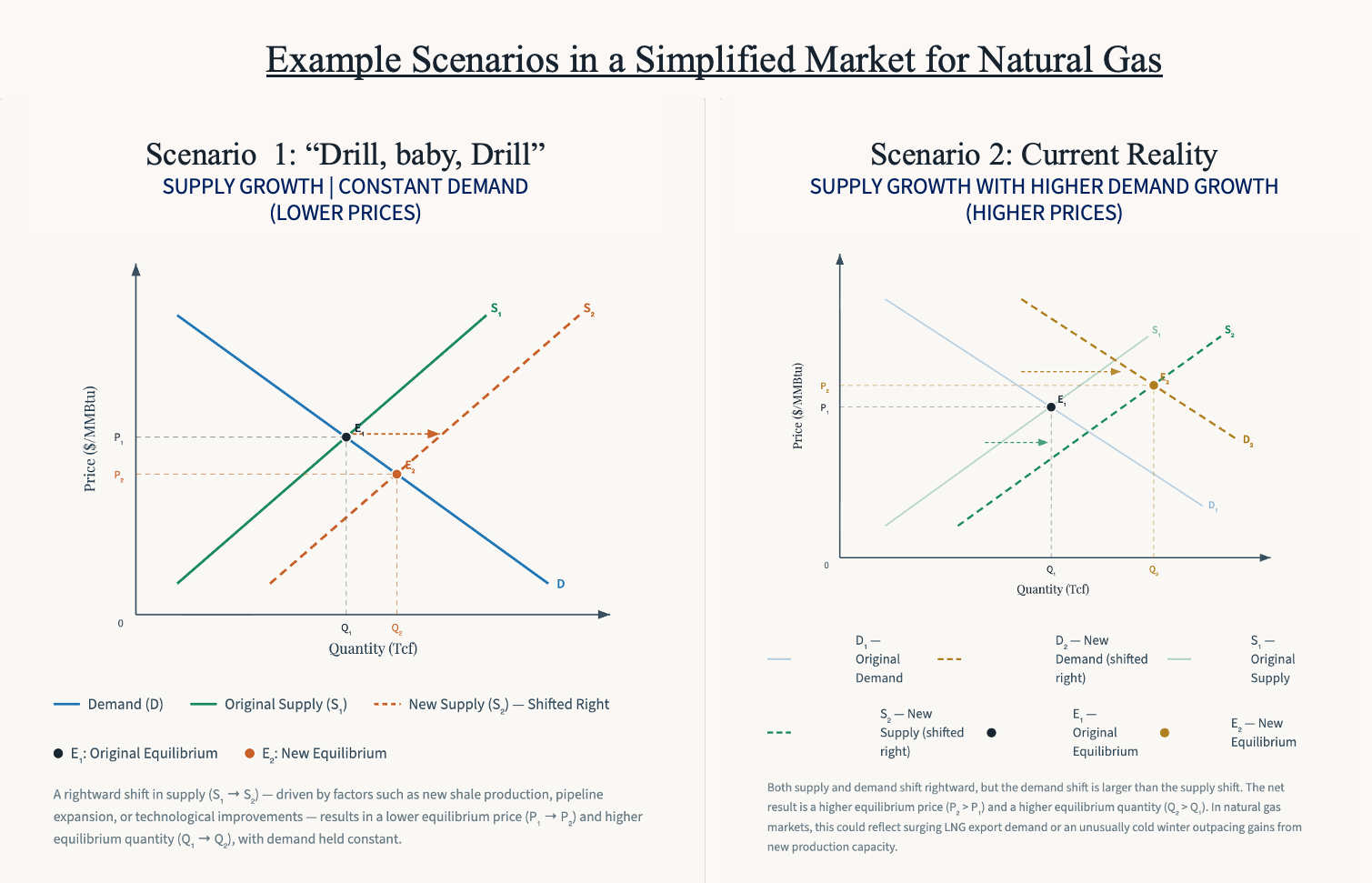

The promise that we can simply drill and frack our way to lower energy prices relies on a bad assumption. While introductory economics suggests that drilling more and increasing the supply of fossil fuels theoretically reduces prices, that is only true if the demand for energy grows more slowly than the supply of gas. These simplified scenarios are illustrated in the figure below, which may give you flashbacks to (or nightmares about) economics class. Nevertheless, their explanatory power is important, and their lesson is critical to debunking this false promise.

In reality, demand is always changing simultaneously with supply. And demand plays a huge role in price determination. This is because 1) demand can (and often does) grow faster than supply chains can ramp up to meet it, and because 2) more drilling costs companies more money, which makes expansion profitable only when demand and prices are already relatively high or rising. This is made even more complex by the fact that oil and gas companies often operate their lowest-cost, highest-output assets first, making additional drilling marginally more expensive when they do have to ramp up to meet more demand. A nuanced, but important point that can be summarized by: drilling more is typically more expensive for companies.

Private energy companies simply aren’t going to voluntarily or preemptively choose Scenario 1 in the image above. If demand were hypothetically constant, “drill, baby, drill” would flood the market for oil and gas, deflate prices, and reduce the company’s own profit margins. Why would they do that?

Such a scenario would be a great windfall for us consumers, but in the real world, production decisions tend to lag price changes. Companies look to increase oil and gas production after demand goes up, which doesn’t really help the average household’s bill. A more realistic example is shown in Scenario 2 above, where demand growth outpaces supply growth and prices still increase, even with more drilling.

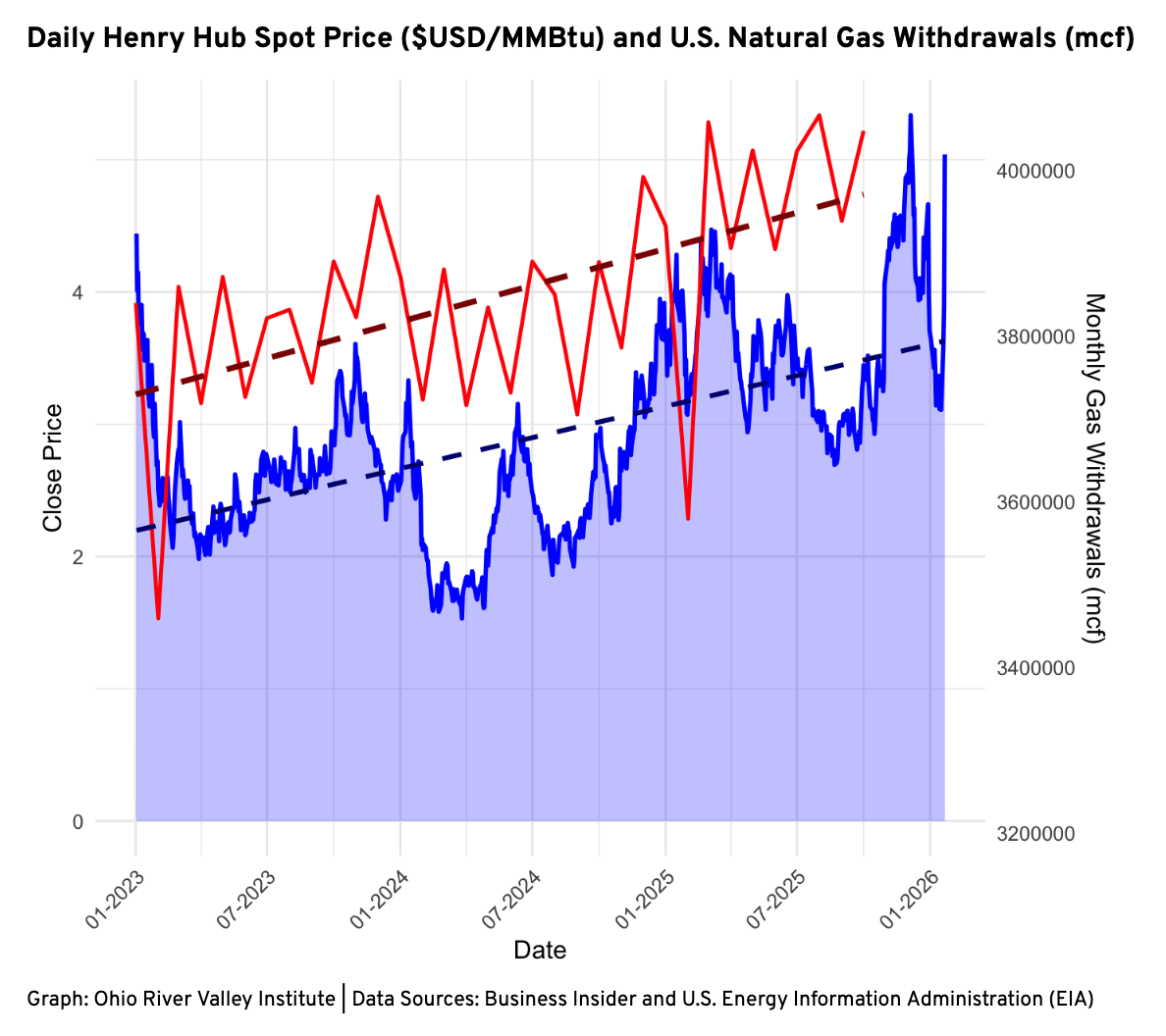

For real-world evidence, look no further than this winter, when natural gas prices have spiked despite a general upward trend in gross natural gas withdrawals (supply) over the last 2 years. In the graph below, I chart the daily Henry Hub spot price in blue from January 2023 to January 21, 2026, and then scale and overlay U.S. natural gas withdrawals in red on the right-hand axis.

The dotted trendlines for the data have a positive slope and suggest that both the supply of gas (either from production or storage) and the price of natural gas are increasing. This is precisely the opposite of the “drill, baby, drill” argument in Scenario 1 that politicians make to justify more fracking and drilling. We are pumping more oil and gas than ever before, yet prices have gone up, not down. Why?

Simply put, demand has gone up faster.

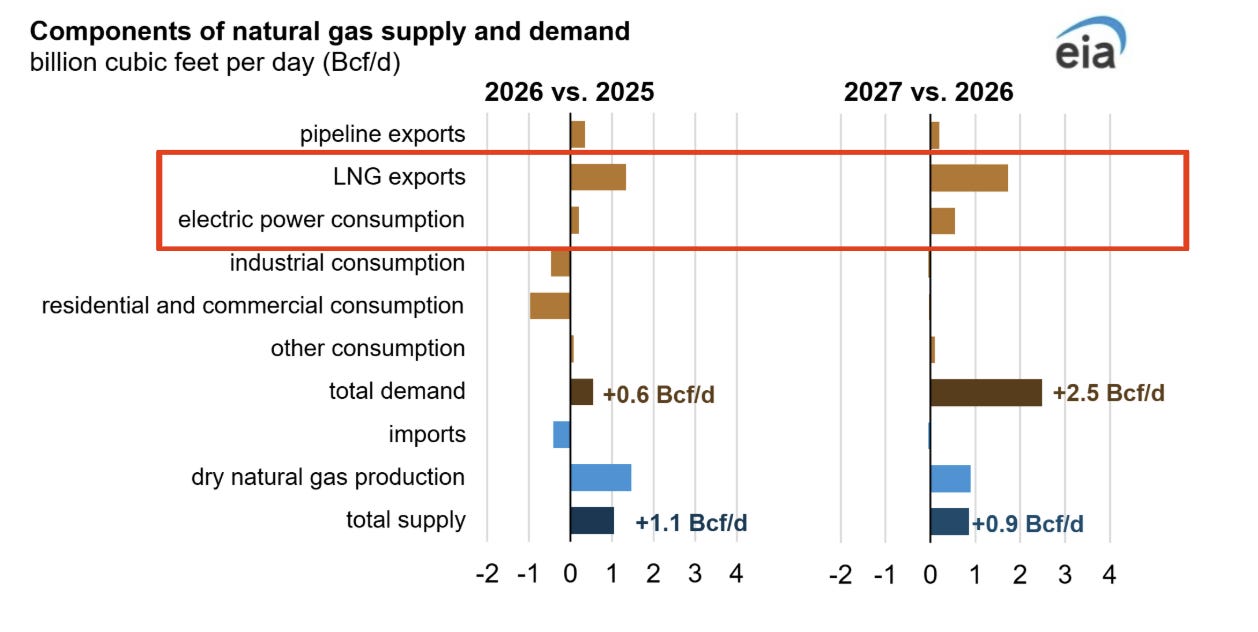

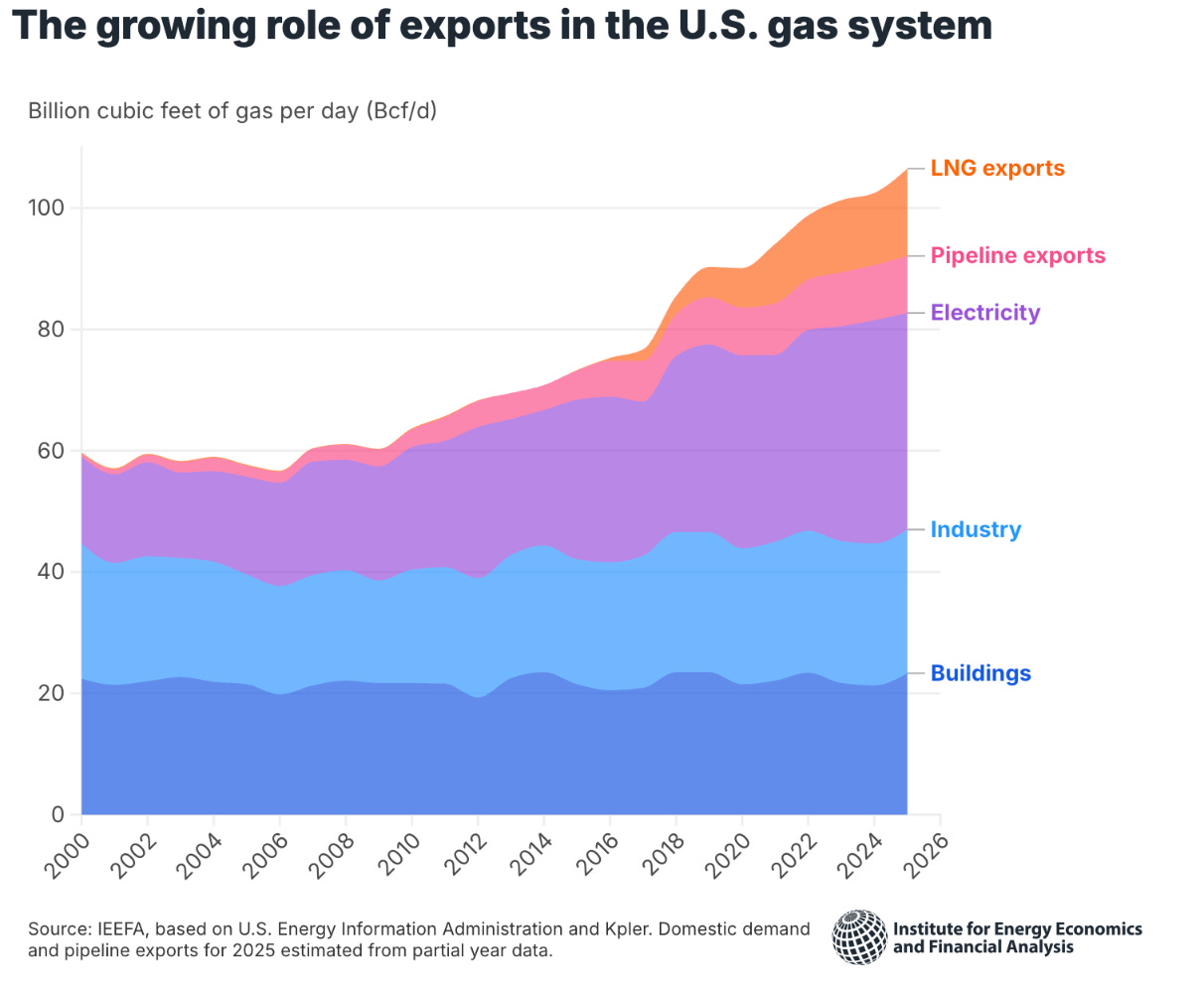

Many factors determine the demand for natural gas, but two likely culprits can be identified in the January 2026 short-term energy forecast from the U.S. Energy Information Administration (EIA), which predicts further rising prices and storage declines in the future.

Electricity generation and pipeline exports have ticked up, but the war in Ukraine and subsequent loss of Russian gas for Western European countries have helped to spur a surge in U.S. liquified natural gas (LNG) exports. The same snake oil salesmen who sold the promise of American energy independence are now selling that same American energy outside of America. And simply fracking for more gas won’t solve our affordability problems if the new gas is sold abroad.

During the Biden administration, pauses on new LNG export terminals were enacted, with President Biden explicitly noting at the time that the impact on energy costs for Americans was a factor that would be evaluated by the government during the pause. The negative environmental and climate impacts of the huge LNG terminals, such as in Cameron Parish, Louisiana, where projects have received billions in state and local subsidies, were also a major consideration in the pause. The Trump Administration has since reversed that pause, and LNG exports are expected to continue to rapidly grow. At a basic level, this means that despite U.S. companies producing more natural gas, Americans will find themselves competing for that new supply on the global market, with Europe and Asia poised to import more LNG than ever in 2026, according to Bloomberg News.

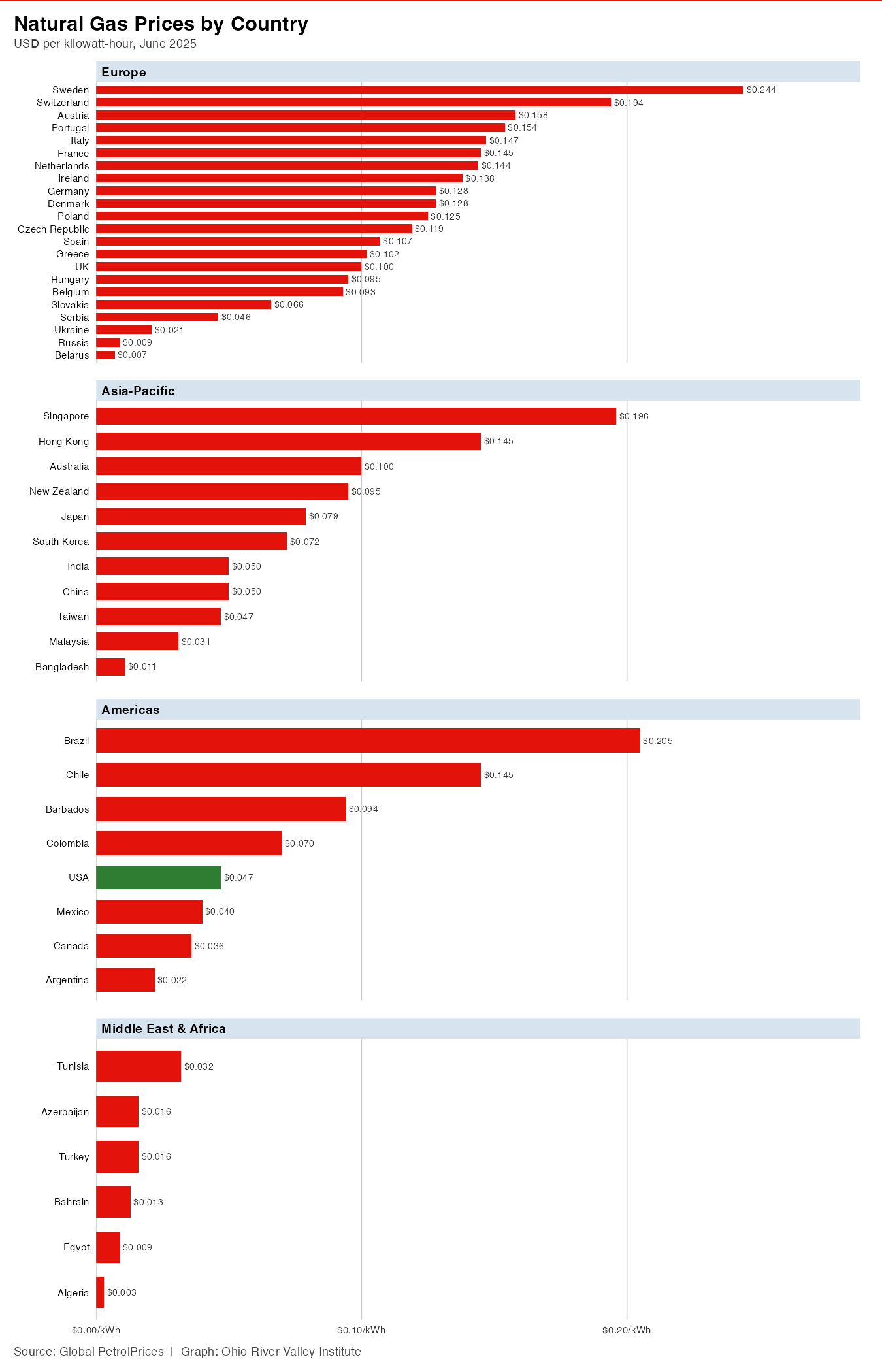

Competing in a global market for gas is problematic for U.S. households, since many of the countries buying American gas are already accustomed to paying much higher prices than U.S. consumers are. The figure below shows a sample of average natural gas prices per kilowatt-hour by country from the middle of 2025. If markets proceed toward an equilibrium “global price,” similar to how oil prices work, we would likely see the world price of natural gas settle in the middle between the U.S. price and the higher prices in Europe and the Asia-Pacific.

In other words, consumers in Europe and Asia could still pay more than what we pay in America, on average, and it would still be a price reduction from what they pay right now. Unless we expect private oil and gas companies to turn down customers willing to pay higher prices, Americans may see their costs bid up as export markets grow.

2. Other administration policies, like promoting data centers, enacting tariffs, and opposing clean energy, are creating headwinds for new capacity construction.

First, the proliferation of electricity-guzzling artificial intelligence (AI) data centers across the United States is increasing overall electricity demand and, thus, demand for natural gas used in power generation. Market forecasts have projected that the AI data center sector will continue to grow, with hundreds of millions of dollars in planned data center investment across U.S. communities over the next four years. This is happening even as local communities struggle with the negative consequences and the current lack of a profitable business model for AI companies.

For example, in Homer City, Pennsylvania, a former coal plant is being repurposed into a natural gas-powered data center complex, which has been heralded as an excellent energy investment with no evidence to suggest it will help lower energy prices for residents. And, despite promising over a thousand jobs, the reality is that even the biggest data center projects rarely employ more than one or two-hundred people once they are built. This has led residents to wonder whether the benefits of the Homer City project will actually flow out of state to large technology companies, in much the same way that the largest economic benefits of fracking have generally left the region. It’s worth noting that, if that is the case, all of the Ohio River Valley states currently abate sales and use tax for data center construction and equipment – a significant possible source of revenue for schools, roads, and public services. Abating local tax dollars for projects where the benefits largely leave the state is just not a sound economic development strategy.

Even if data centers are required to generate their own electricity “behind the meter” using private power plants, as the President vaguely announced in his recent State of the Union Address, they would still need to burn natural gas to make that electricity. Thus, even if data centers don’t directly or immediately increase electricity costs on the grid, their additional need for natural gas could still contribute to higher fuel costs for the rest of our power plants. We haven’t seen fuel costs drive up prices significantly yet, with the majority of current electricity price increases being related to transmission and distribution buildouts. But, in time, if the data center buildout materializes at a large scale, we could end up with even higher electricity rates.

Second, even if the future baseline grid load is met by natural gas, renewable energy and storage offers a potential pressure release valve for times of global volatility. While it is a popular political talking point to say that the costs of the renewable energy transition have generally caused higher utility prices, there’s little evidence to support the claim. While generation costs have been relatively flat, transmission and infrastructure buildouts, large capital investments in aging coal plants, geopolitical turmoil, and a lack of supplementation from renewable energy have largely created our region’s energy affordability crisis.

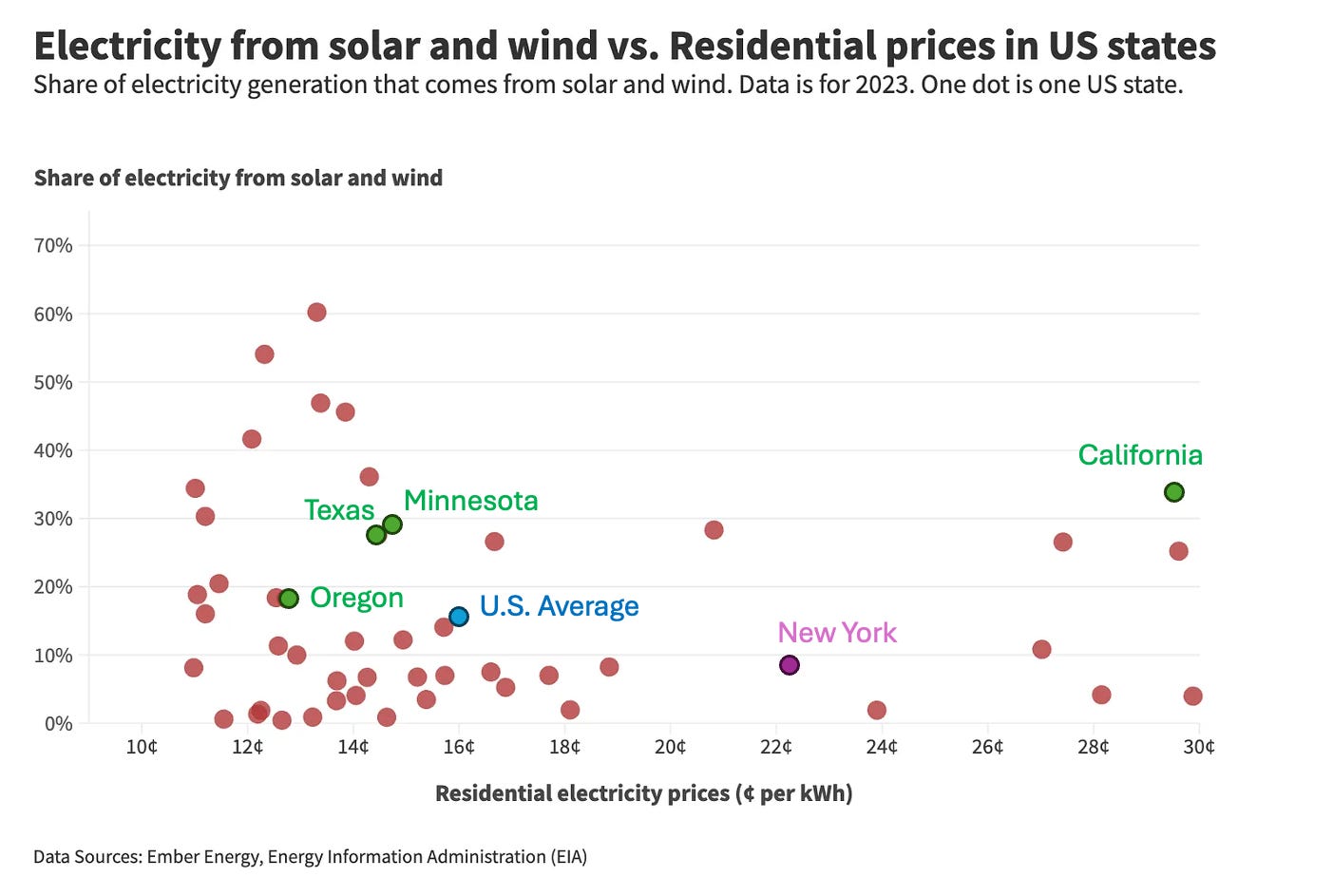

In fact, states with some of the largest shares of their electricity coming from renewable sources have maintained lower consumer prices than areas of the country rich in oil and gas, as shown in the figure below.

I caution that this feat isn’t replicable at the same cost everywhere; the Southwest is much sunnier, and the plains states are much windier than the Midwest, reducing the required capital costs with fewer panels or turbines required to generate the same amount of energy more consistently. A few things stand out, however. First, a few pretty populous states like Texas, Oregon, and Minnesota have achieved below-average residential electricity rates with above-average shares of their electricity coming from wind and solar. And Minnesota and Oregon can hardly be accused of being perpetually sunny places.

I also highlight California on the chart, in the interest of transparency. While it is the most populous state in the country with one of the largest renewable shares of electricity production, it has been far above the average U.S. electricity rate since the 1980s. Explanations for this trend that predate renewable energy adoption include aging infrastructure, wildfire mitigation costs, and pricing by privately owned utilities. It’s also worth noting that Californians also use less electricity than the average American, likely owing to some combination of the temperate climate and energy efficiency measures. I note this because I am not arguing that renewable energy is a “silver bullet” for energy prices or reliability, but it is generally cheaper to build in the short term and a strategic component of long-term price stability.

Renewable energy also has a feature that works to the advantage of consumers in a globalized economy: it is largely consumed locally. Electricity from solar arrays or wind turbines isn’t easily loaded on ships and sold on global markets like natural gas or oil. That means that, when it comes to renewables, Americans could truly be energy independent and wouldn’t directly compete in a global market with foreign consumers. It also means that the price of renewable electricity doesn’t have to factor in the billions of dollars in capital spent by companies to build expensive LNG terminals.

Recent empirical work has also found that increasing renewable energy’s share of power generation in importing countries reduces the overall global demand for LNG, suggesting that they are at least partial substitutes for consumers. This means that investment in renewable energy is another plausible mechanism to reduce overall natural gas demand and lower the price of the gas that America needs at baseline. By phasing out federal funding and tax credits for investments in clean power generation and decarbonization in last year’s One Big Beautiful Bill Act and by promoting the construction of new mega gas-fired power plants, the administration is kicking the ball into its own net, so to speak, when it comes to building an affordable energy future.

The final headwind that the administration has created for itself is the haphazard and broad implementation of tariffs. Tariffs raise prices by either making imports more expensive or by allowing domestic producers to raise their prices to match the new, higher import prices. The Trump Administration’s tariffs went into effect in a staggered fashion, largely in April 2025, May 2025, or August 2025, depending on the industry and country.

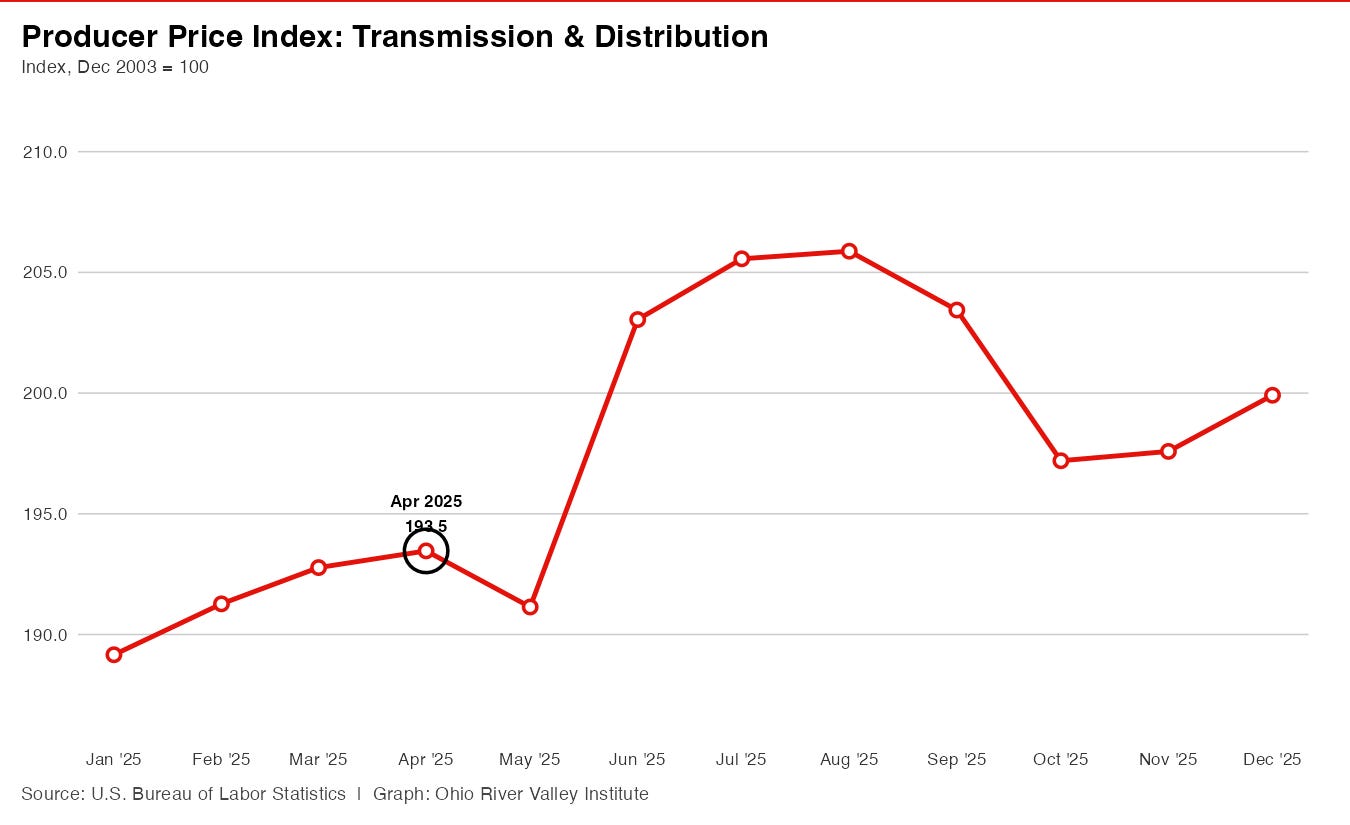

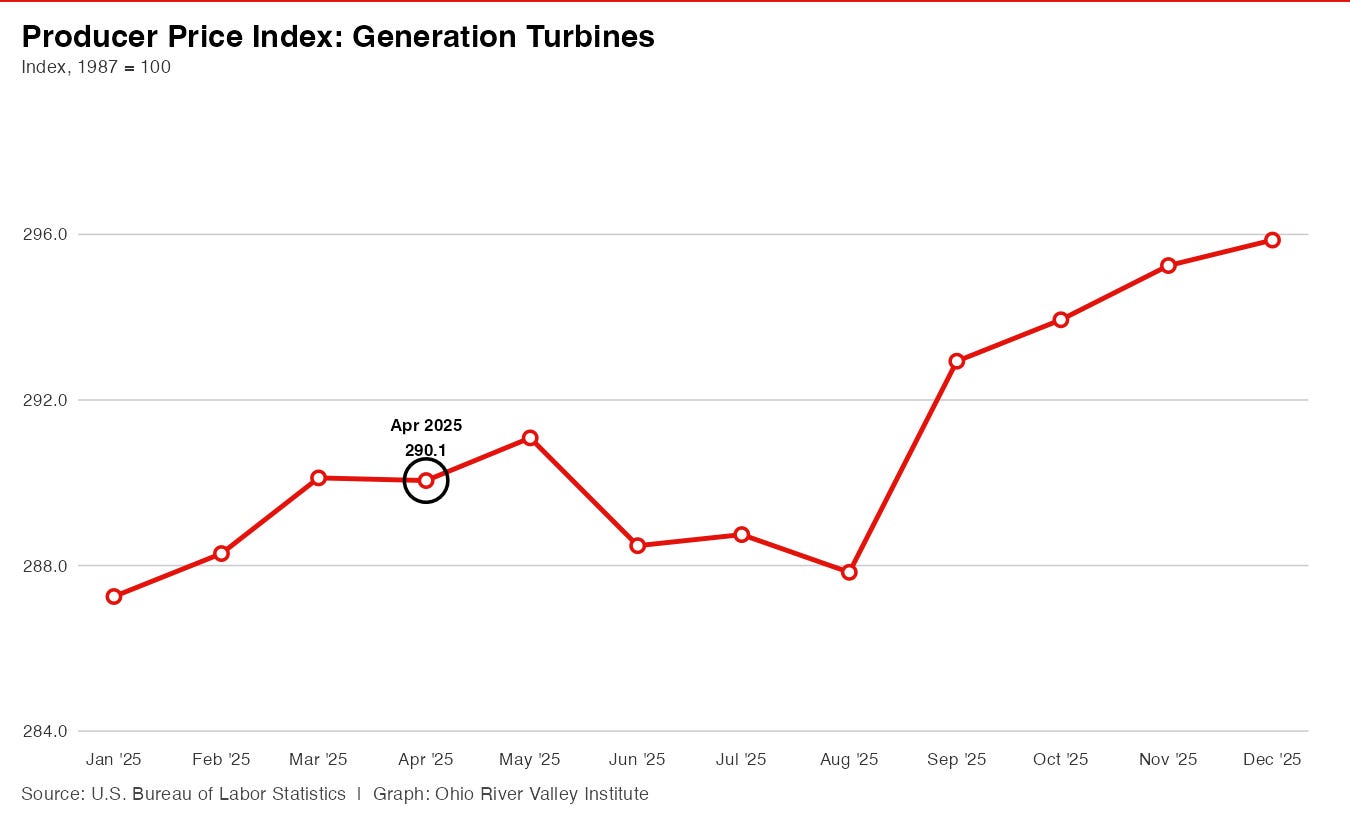

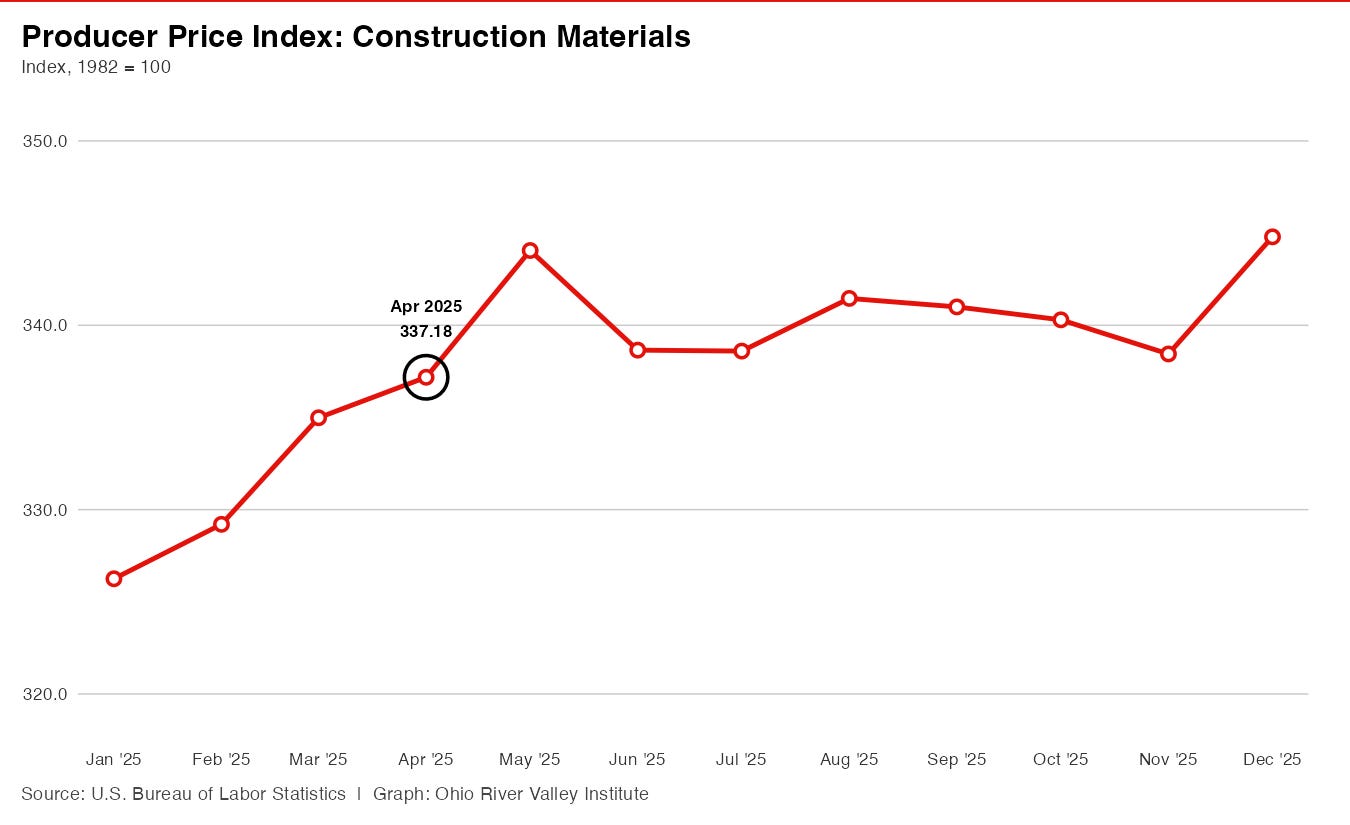

I noted earlier that most of the cost of electricity price hikes has been due to transmission and distribution construction—the transformers and power lines that process the electricity generated from power plants and deliver it to homes, businesses, and factories. The graphs below look at the producer price index (prices received by the seller) for three related industries: electricity transmission, control, and distribution, turbine generator sets, and construction material manufacturers.

In all three cases, large price spikes begin after April, May, or August in 2025, which generally corresponds with the administration’s tariffs taking effect. This suggests that the administration’s tariffs have at least partially contributed to our rising utility costs by making the construction of new gas generation and new transmission and distribution infrastructure more expensive. Evidence shows that these higher costs for utility companies are ultimately passed on to household and industrial consumers in the form of higher prices, fees, or riders.

In a sense, while the administration may say that they are pursuing policies to “unleash American energy” with their left hand, they are rapidly attaching new chains with their right hand through a variety of misguided policies. These include:

Promoting LNG export terminal expansion to sell more natural gas abroad.

Encouraging data center construction by tech companies, which compete privately for natural gas, even with behind-the-grid electricity generation.

Ending incentives for investment in less-volatile, cheaper, and locally consumed renewable electricity.

Enacting global tariffs that raise the costs of the materials and equipment needed to grow and expand our electric grid.

Combined, these policies mean that even if we “drill, baby, drill,” the gas that we produce will very likely either be sold on a more expensive global LNG market or the plants, transformers, and powerlines needed to convert it into usable electricity will cause more prices increases, offsetting the effects of extra production.

The truly bleak scenario is the one where these forces all work simultaneously, perfectly aligning in the future to increase gas costs, raise construction costs, delay timelines, and close the door on alternative, supplemental sources of local clean energy. If you’re a private oil and gas company or a shareholder, this may be just what the doctor ordered, but for the rest of American households and businesses, this policy concoction will likely become more poison than cure, leading to even higher utility bills in the future.